The US stock market is home to some of the most famous stocks in the world, such as McDonald’s Corp (NYSE: MCD), Starbucks Corporation (NASDAQ: SBUX), and Nike Inc (NYSE: NKE).

Many may not know, but the US market also contains the world’s biggest companies by market capitalisation. The top four largest companies are (as of 8 September 2022):

- Apple Inc (NASDAQ: AAPL),

- Saudi Arabian Oil Co. (or Saudi Aramco listed in Saudi Arabia),

- Microsoft Corporation (NASDAQ: MSFT), and

- Alphabet Inc (NASDAQ: GOOGL) (NASDAQ: GOOG).

With the stock market correcting in the early part of the year, the share prices of those US-listed companies are in negative territory year-to-date.

As such, investors may be wondering:

“Is there value in the largest companies, and is it worth buying shares of them for the long term?”

Let’s find out more right here.

Apple Inc

- Market Cap: USD 2.49T

- Price / Earnings: 25.29

- Current Yield: 0.41%

- Return On Equity: 30.98%

Apple designs a wide variety of consumer electronic devices, including smart phones (iPhone), tablets (iPad), computers (Mac), and smart watches (Apple Watch), among others.

The iPhone makes up most of Apple’s total revenue, and the company generates roughly 40% of its revenue from the Americas, with the remainder earned internationally.

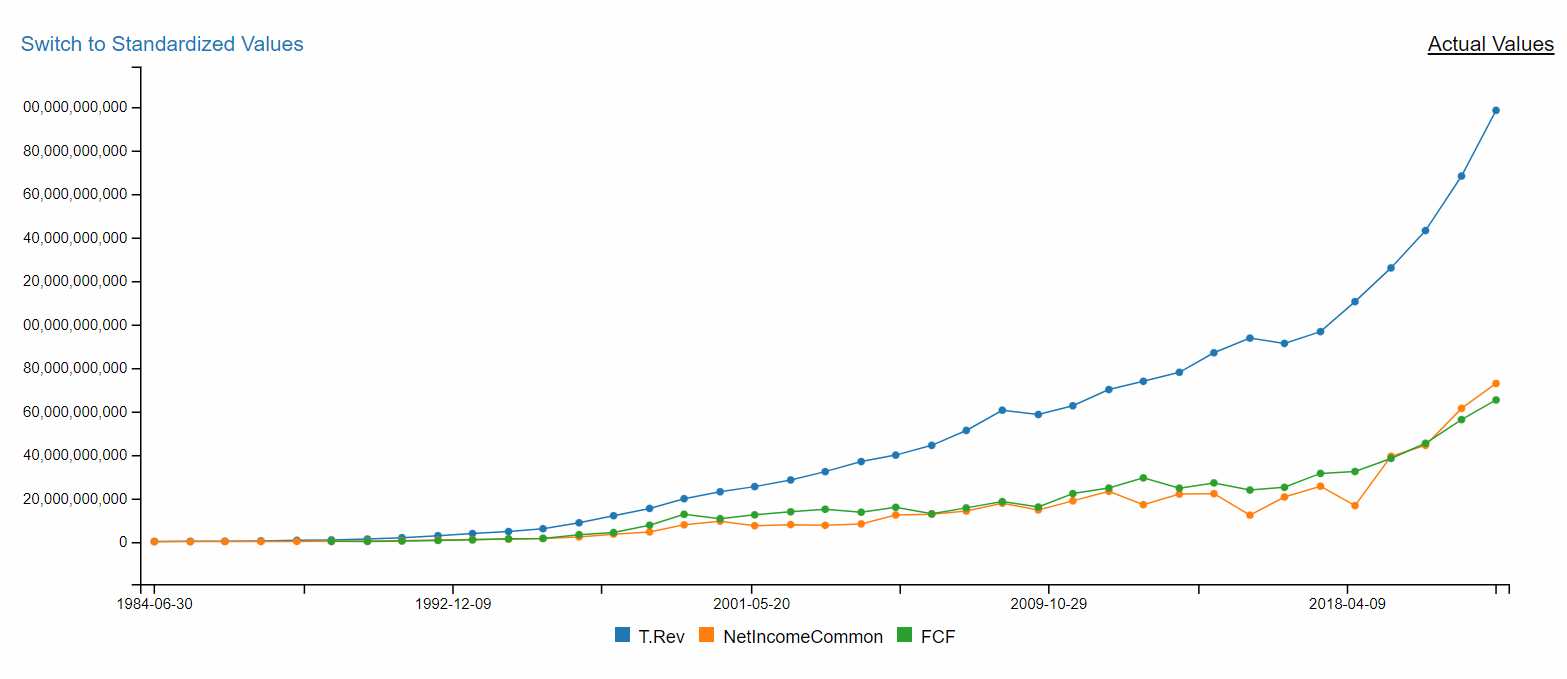

Over the past many years, Apple has seen strong growth in its business, as seen in the chart below:

More specifically, Apple’s revenue has grown over the past five years from US$229.2 billion in fiscal 2017 to US$365.8 billion in fiscal 2021. Likewise, its net profit and free cash flow have also stepped up consistently.

Apple has been able to grow its business strongly due to its brand appeal. The company’s strength has won over even Warren Buffett.

The famed investor mentioned the following about Apple during Berkshire’s 2021 annual general meeting (AGM):

“And there’s an installed base of people, and they get satisfaction rates of 99%. … I mean the brand and the product is — it’s an incredible product. So a huge, huge bargain to people. I mean, the part that plays in their lives is huge.”

It’s just difficult for a competitor to topple Apple from its top perch.

For Apple’s latest quarter (fiscal 2022 third quarter ended 25 June 2022), it continued to do well, posting a revenue increase of 2% year-on-year to US$83 billion, setting a new June quarter record.

Luca Maestri, Apple’s chief financial officer, explained his company’s latest performance in its earnings release (emphases are ours):

“Our June quarter results continued to demonstrate our ability to manage our business effectively despite the challenging operating environment. We set a June quarter revenue record and our installed base of active devices reached an all-time high in every geographic segment and product category. During the quarter, we generated nearly $23 billion in operating cash flow, returned over $28 billion to our shareholders, and continued to invest in our long-term growth plans.”

The large installed base of active devices has also allowed Apple to sell more of its services to users. Such services include its cloud service iCloud, Apple TV+, and Apple Music, and they provide the company with recurring revenue.

Services revenue has been a growing segment for Apple. Services contributed 11% of total sales in FY2016, and the contribution has increased to 19% in FY2021.

Furthermore, Apple has consistently repurchased its shares and dished out cash to its shareholders through dividends. With a large cash pile and growing free cash flow, it makes sense for Apple to buy back its shares and reward its shareholders with dividends. A decreasing share count also means that shareholders will get to own more of the company without doing anything.

By buying back its shares when the conditions are right, Apple can increase its per share figures, such as earnings per share and free cash flow per share, making the company more valuable. A higher per share growth, with all things being equal, is always valued by investors.

At Apple’s share price of US$154.53, it has a price-to-earnings (P/E) ratio of around 26x, while its 5-year average stands at 24x. This could suggest that the Apple stock is currently slightly overvalued, but it could also be worth paying up for a quality company.

Microsoft Corporation

- Market Cap: USD 1.89T

- Price / Earnings: 26.11

- Current Yield: 0.69%

- Return On Equity: 48.72%

Microsoft develops and licenses consumer and enterprise software. It is known for its Windows operating systems and Office productivity suite.

The company is organised into three business segments:

- Productivity and Business Processes (legacy Microsoft Office, cloud-based Office 365, Exchange, SharePoint, Skype, LinkedIn, Dynamics),

- Intelligence Cloud (infrastructure- and platform-as-a-service offerings Azure, Windows Server OS, SQL Server), and

- More Personal Computing (Windows Client, Xbox, Bing search, display advertising, and Surface laptops, tablets, and desktops).

For Microsoft’s fourth quarter ended 30 June 2022 (FY22 Q4), its revenue increased by 12% year-on-year to US$51.9 billion, while its net income grew 2% to US$16.7 billion.

Amy Hood, Microsoft’s executive vice president and chief financial officer, commented:

“In a dynamic environment we saw strong demand, took share, and increased customer commitment to our cloud platform. Commercial bookings grew 25% and Microsoft Cloud revenue was $25 billion, up 28% year over year. As we begin a new fiscal year, we remain committed to balancing operational discipline with continued investments in key strategic areas to drive future growth.”

For the whole of FY2022, Microsoft’s revenue increased by 18% year-on-year to US$198.3 billion, and its net profit grew 19% to US$72.7 billion.

Over the long term, Microsoft has delivered the goods as well.

We can see that critical metrics of revenue, net profit and free cash flow have all increased over the past many years.

Future growth for Microsoft can come from its Azure cloud computing business and its enterprise software segment as people go increasingly digital in a hybrid working environment post-pandemic.

According to estimates from Synergy Research Group, Azure’s market share in the worldwide cloud infrastructure market stood at 21% in the second quarter of 2022, coming in second behind Amazon’s AWS. There’s potential for Azure to increase its cloud market share if it continues executing well.

At Microsoft’s share price of US$253.25, its P/E ratio is around 26x, while its 5-year average stands at 37x. This could mean that Microsoft is currently undervalued, and it might be worth taking a second look at this company.

Alphabet Inc

- Market Cap: USD 1.41T

- Price / Earnings: 19.78

- Current Yield: 0%

- Return On Equity: 6.28%

Alphabet is a collection of businesses, the largest of which is Google.

Alphabet reports Google in two segments – Google Services and Google Cloud. It also reports all its non-Google businesses as Other Bets, which include technology outfits that are in the early stages of their business cycles.

Advertising makes up the bulk of Alphabet’s revenue. For FY2021, the company made US$209.5 million in advertising revenue (or 81% of total revenues).

Alphabet’s wide economic moat where it has a network effect, and strong brand have allowed it to grow its financials well in the past, as seen from the chart below:

From FY2017 to FY2021, Alphabet’s total revenue has increased consistently from US$110.9 billion to US$257.6 billion, while its net profit grew from US$12.7 billion to US$76.0 billion. With that, the company’s free cash flow has stepped up too.

For its 2022 second-quarter, Alphabet continued its strong showing. Alphabet’s total revenue grew 13% year-on-year to US$69.7 billion and the operating income inched up by 0.5% to US$19.5 billion.

Sundar Pichai, Alphabet’s chief executive, mentioned:

“In the second quarter our performance was driven by Search and Cloud. The investments we’ve made over the years in AI and computing are helping to make our services particularly valuable for consumers, and highly effective for businesses of all sizes. As we sharpen our focus, we’ll continue to invest responsibly in deep computer science for the long-term.”

In the short term, there could be headwinds for Alphabet’s advertising business, given the uncertain global economic outlook. However, over the long run, there’s room for the company’s ad business to grow.

According to eMarketer, the global digital marketing expenditure is expected to increase from US$380.8 billion in 2020 (59% of total media ad spending) to US$785.1 billion in 2025 (72% of total media ad spending). The growth translates to an annualised growth of around 15.6%.

With Google being the most dominant platform for advertisers in the digital ad market, Alphabet still has plenty of room to grow in its worldwide market.

At Alphabet’s share price of US$107.48, it has a P/E ratio of about 20x, and its 5-year average is 33x. It’s surely worth researching further into Alphabet to take advantage of the undervalued stock price.

StocksCafe, an investment research and portfolio tracking tool, will come in handy as you look further into Apple, Microsoft and Alphabet. Be sure to check out StockCafe’s free trial with plenty of features.

Written by Sudhan P, in collaboration with StocksCafe.

Disclaimer: The content in this article (the “Information”) is not and shall not be construed as investment advice. This Information is meant to be informative and for general purposes only. Investment involves risk. Past performance is not indicative of future performance. Investors should refer to the offering documentation of the product(s) for detailed information (including risk factors) prior to investing in the product(s). If you have any query on the above information or any product offering documentation, you should seek independent professional advice.