Sea Limited was established in Singapore in 2009 and is a leading tech company, with businesses in Digital Entertainment, E-commerce, and Digital Financial Services. As the stock market continues to crash as we enter 2022, the sector which is most adversely affected is the technology sector. If an investor is not knowledgeable enough, it could be both daunting and risky to venture into this space.

The stock of Sea Limited has collapsed dramatically since late 2021, much to the dismay of its investors. From 2020 to 2021 a run-up was observed, but in October 2021, the stock started seeing a downfall, and subsequently plummeted almost 80% from its highs. It appears that the market has been pricing in slow growth due to inflation and recession fears in the Southeast Asia region.

From the chart above, we can see that Sea’s stock performance features a steep decline, which is in sharp contrast to the regional ETFs of the markets that the company operates in, like QQQ or SPY. Despite the performance of the company moderating over the past year, the overall 3-year performance is still very healthy, up 202.4%.

Performance of the Business in Q2 2022:

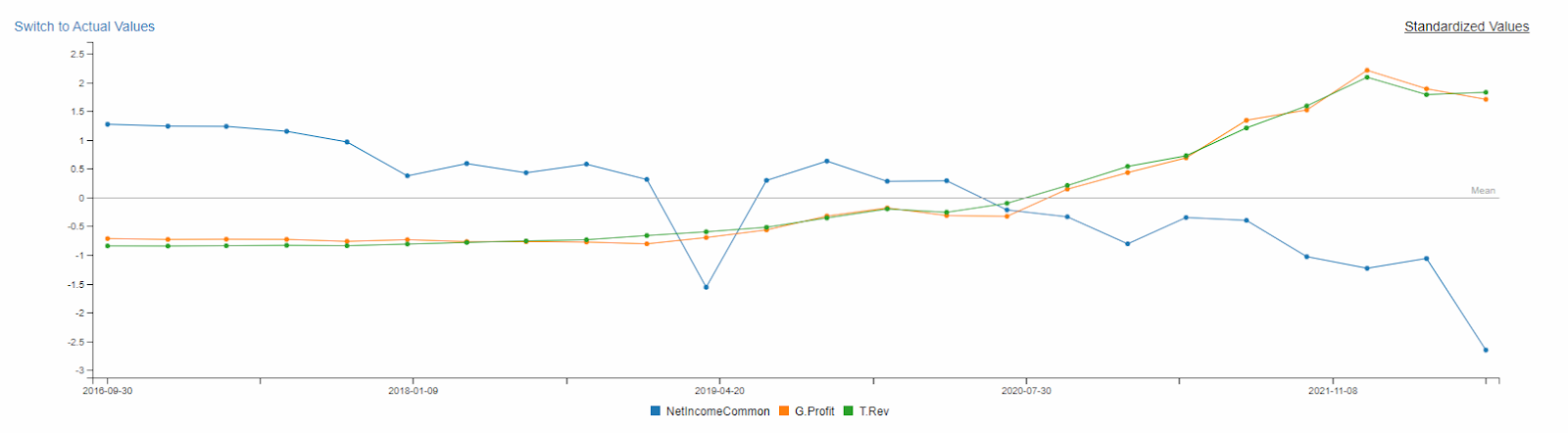

As we can see from the chart above, Sea saw a huge increase in net losses for Q2 2022, and its gross profits continue to fall quarter over quarter. On a year-on-year basis, its total GAAP revenue did grow by 29% to $2.9 billion, and its gross revenue grew by 17.1% to $1.1 billion. However, the net loss incurred for Q2 2022 was $931.2 million, as compared to $433.7 billion in Q2 2021.

The revenue owing to the e-commerce segment of the business, Shopee, was $1.7 billion (showing a 51.4% year-on-year growth). The adjusted EBITDA was $648.1 million in Q2 2022 as compared to $579.8 million in Q2 2021.

The GAAP revenue owing to the digital entertainment segment, Garena, was reported to be $900.3 million in Q2 2022 as compared to $1.0 billion for Q2 2021. Subsequently, the adjusted EBITDA was $333.6 million as compared to $740.9 million.

Coming to the third business segment of digital financial services, SeaMoney, the revenue was reported to be $279.0 million (with a 214.4% year-on-year growth) and adjusted EBITDA is $111.5 million in Q2 2022, as compared to $155 million in Q2 2021.

From the above, we can definitely see that its digital entertainment segment, Garena, is the only one with a net decrease in growth year-on-year, while its other two business segments are growing rapidly. As Garena is already a mature segment of the business, it can be expected that its growth will slow down and eventually stagnate over time.

Past 5 years’ Performance:

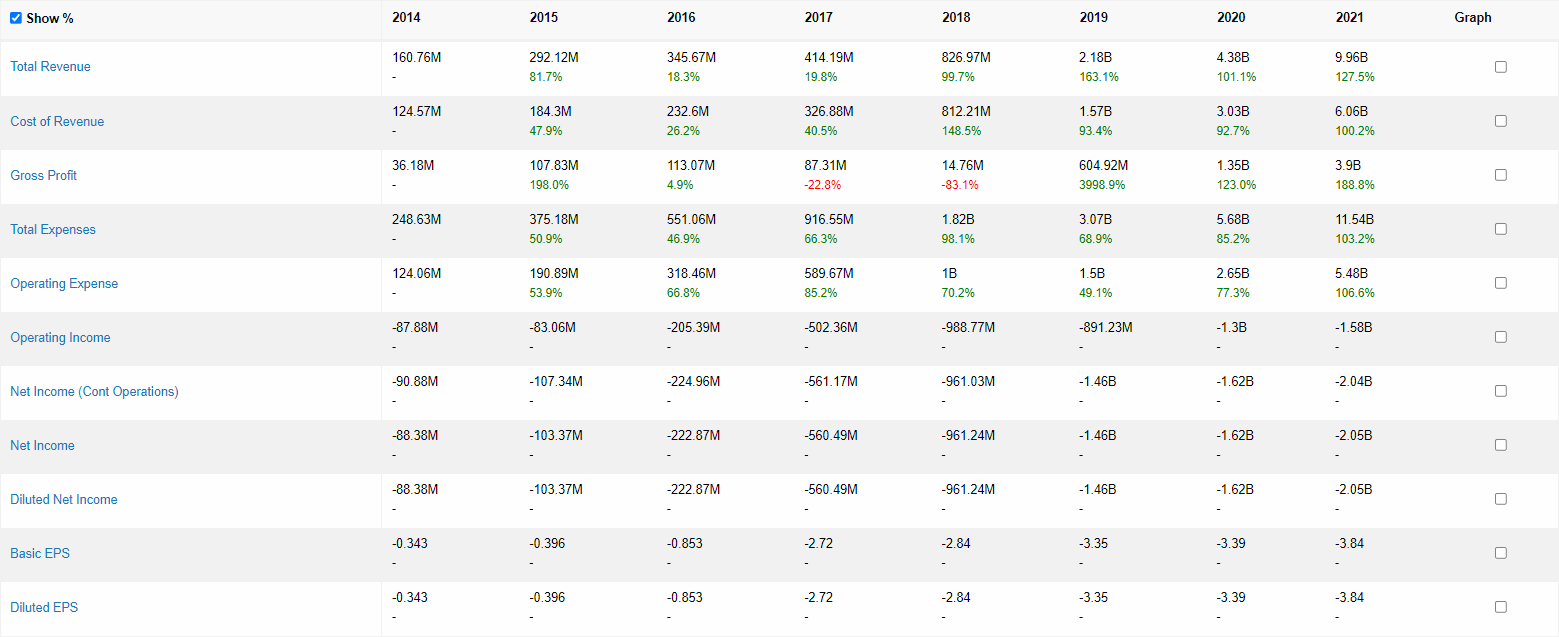

Looking at the earnings trend, we can see that Sea has been able to grow their top line very aggressively at a CAGR of 85.49% over the past 5 years. Even with this very strong growth, Sea has remained unprofitable as its losses have risen at a rate of 28% per year over the past 5 years.

Despite this, investors are still hopeful that Sea will soon turn profitable as the company did mention a path to profitability in its FY2021 Full Year Results. In the earnings release, Sea mentioned that they expect Shopee to achieve positive adjusted EBITDA by 2022 and SeaMoney to achieve positive cash flow by 2023. On top of that, they believe that by 2025, the cash generated by Shopee and SeaMoney can self-fund their long-term growth.

The Dependency on Garena:

Garena, which is Sea’s gaming segment, developed one of the most interesting games, Free Fire, that is being played all around the globe right now. Their vision is to normalize eSports gaming as much as they can to let people turn their passion into a profession. In 2019, Free Fire was the most downloaded game globally and the top-grossing in Southeast Asia and Latin America and as of May 2021, Garena’s Free Fire had over 150 million daily active users globally.

Garena is Sea’s cash generating machine and thus Sea is overly dependent on Garena. However, as the earnings ratios and operating metrics showed a downturn, we now know why this is a serious issue which needs to be looked into. In the Q4 2021, Garena reported a revenue of $1.1 billion. Yearly, the quarterly bookings rose by 7% but in the second and third quarters of 2021, it fell even lower than $1.2 billion. The quarterly active users (QAU) rose by 7% yearly but fell in the previous quarter. These weak metrics show that Garena’s growth has hit a plateau.

According to some analysts, Sea is reported to show a revenue growth of less than 40% in 2022. Garena reported bookings of $4.6 billion in 2021 and in 2022 it is expected to show much lower bookings of $3 billion.

Shopee:

Sea’s Ecommerce platform, Shopee, was launched in 2015 and is currently the leading e-commerce platform in Southeast Asia and Taiwan. The marketplace is intuitive to use and user-friendly. It not only provides the best experience to the customers, but many people are using this platform to build their own businesses.

Shopee’s only real competitor in Singapore is Lazada, which is owned by Alibaba Group. Both eCommerce platforms sell a wide range of products as well as give out discounts and vouchers almost weekly. As of 2021, Shopee holds a strong market share across many markets in Southeast Asia such as Indonesia (38.88%), Vietnam (32.33%), Thailand (50.57%), Philippines (62.38%), Malaysia (66.44%) and Singapore (40.46%).

Shopee’s revenue in Q1 2022 was $1.59 billion, but it fell to $1.52 billion in the second quarter. Shopee is generally labeled as Sea’s not-so-profitable e-commerce unit. The revenues in the 2 quarters of 2022 fell because of heavy logistics and marketing expenses which led to $810 million in losses (that is $131 million less than the previous quarter).

The company’s expected full-year revenue was reported to be in between $8.5 billion and $9.1 billion, the reason being “elevated macro-uncertainties”, as cited by the company.

SeaMoney:

Sea Limited’s fastest growing segment is their digital finance payment, also known as SeaMoney. In Southeast Asia, SeaMoney is the largest digital payment service used for financial purposes. It includes features like mobile wallet, payment processing, AirPay, ShopeePayLater, and many other innovations. SeaMoney is Sea’s first step into the financial technology (FinTech) space and it has been a great move thus far. Along with Shopee, as SeaMoney scales and strengthens their market leadership position, they will continue to enjoy operating leverage and efficiency gain.

Conclusion:

Looking at how far Sea has come – growing Shopee’s market share in such a short period of time, and now obtaining the Digital Full Bank license in Singapore which could come in handy in collaboration with SeaMoney – the company does offer a huge potential for growth if all the stars align correctly.

However, it might just be too big of an “if”, when you take into consideration its current valuation as well as the ongoing state of the economy.