Temasek is one of two sovereign wealth funds in Singapore. Since its inception in 1974, some 48 years ago, Temasek’s total shareholder return (TSR) stood at an annualized rate of 14%, which is commendable. In comparison, the MSCI World Index has posted a yearly return of around 8% since 1987. Even though the time frame is not the same, Temasek has managed to beat the average market returns over the long run.

Recently, the investment company announced its financial results for the year ended 31 March 2022. On a 1-year basis, its TSR was positive at 5.8%, amid a volatile market in general. And its net portfolio value hit a record S$403 billion as of end-March 2022, showing steady growth since its heyday where its initial portfolio stood at a mere S$354 million.

Even though Temasek is a Singapore-based investment entity, its ambitions are global. 73% of its portfolio is invested outside of the city-state, with China taking up the most of the pie at 22%.

Let’s explore three of Temasek’s major investments that are listed in the US.

Airbnb Inc

Now that global economies have opened up after an almost a two-year hiatus, many people are once again flying around the world to scratch their travel itch.

One big beneficiary of this pent-up travel demand is Airbnb Inc.

Airbnb went public in December 2020 and it was probably one of the most highly-anticipated initial public offerings (IPO) of that year.

Airbnb operates a global marketplace business, where hosts offer guests stays and experiences on its platform. Almost all of Airbnb’s revenue comes from stays booked on the Airbnb platform.

In 2020, Airbnb’s revenue was hit badly due to the Covid-19 pandemic. As seen from the table below extracted from StocksCafe, the marketplace’s revenue in the 2020 first-quarter plunged 82.5% and in the 2020 second-quarter, tumbled another 60.2% (both on a trailing twelve months basis).

However, since the first quarter of 2021, on a trailing 12 months basis, Airbnb’s revenue has been on an uptick, almost doubling from US$3.42 billion for the quarter to US$6.61 billion in the latest quarter.

Airbnb also posted a net profit of US$801.4 million on a trailing twelve months basis up till the first quarter of 2022, reversing the losses it has seen in many quarters of the past.

For the latest quarter, Airbnb’s revenue stood at US$1.5 billion, increasing by 70% year-on-year showing the strength of the travel rebound.

The company said that it exceeded 100 million Nights and Experiences Booked, its largest quarterly number ever.

Nights and Experiences Booked is a key measure of the scale of Airbnb’s platform, which in turn drives its financial performance. The metric represents the sum of the total number of nights booked for stays and the total number of seats booked for experiences, net of cancellations and alterations that occurred in that period.

Airbnb has another metric called gross booking value (GBV), which is the dollar value of bookings on its platform and includes host earnings, service fees, cleaning fees, and taxes, net of cancellations and alterations that occurred during that period. Included in GBV is Airbnb’s revenue, which is the service fees, after deduction of incentives and refunds, charged to its customers (both hosts and guests).

GBV of US$17.2 billion and revenue of US$1.5 billion in the 2022 first-quarter were both over 70% higher than the pre-pandemic 2019 first-quarter levels.

In its 2022 first-quarter shareholder letter, Airbnb said:

“Two years since the pandemic began, a new world of travel has emerged. Millions of people are now more flexible about where they live and work. As a result, they’re spreading out to thousands of towns and cities, staying for weeks, months, or even entire seasons at a time. Through our adaptability and relentless innovation, we’ve been able to quickly respond to this changing world of travel. Now, two years into the pandemic, Airbnb is substantially stronger than ever before.”

Airbnb should bounce back strongly as people fulfil their desires to travel once again. For those who are looking to own a travel-related stock now that the world has reopened its borders, Airbnb could be a good addition to your portfolio.

Currently, Airbnb is trading at a share price of US$102.20, and that translates to a price-to-sales (P/S) ratio of 10x. Since Airbnb’s IPO, it had an average P/S of around 20x, so its current valuation could suggest that the business is undervalued.

Alibaba Group

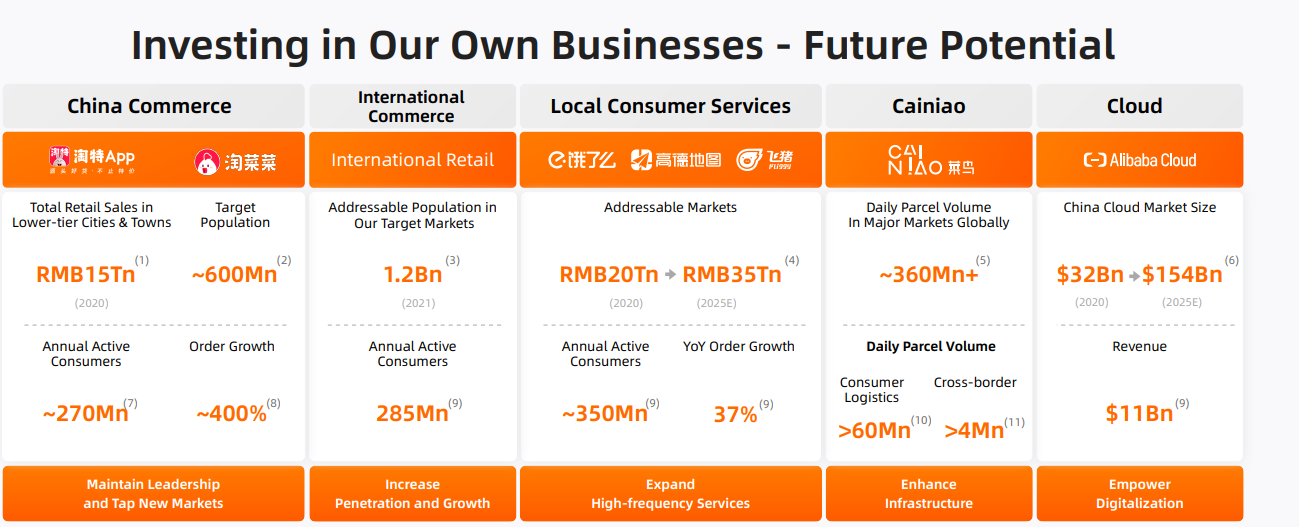

Alibaba Group is the world’s largest online and mobile commerce company as measured by gross merchandise volume.

Some of the businesses under its umbrella include:

- Alibaba.com, China’s leading integrated international online wholesale marketplace

- Taobao, China’s leading social commerce platform

- TMALL, the world’s leading third-party online and mobile commerce platform

Alibaba also runs a cloud service called Alibaba Cloud, which is Asia Pacific’s leading infrastructure-as-a-service (IaaS) provider by revenue.

China technology companies, in general, have been in a negative light due to the regulatory crackdown in the country. However, in March this year, it was reported that Chinese Vice-Premier Liu He is making a push to stabilise the battered financial markets, promising to ease the regulatory crackdown.

That, in turn, should lift investor sentiments in the China tech sector, including Alibaba.

Since 2011, Alibaba’s overall business has grown at a strong clip, with both revenue and net profit seeing steady growth.

Over the long term, Alibaba still has the potential to grow in the e-commerce and cloud sectors due to the size of the China market, not forgetting the international growth of the company. In my opinion, for those who want to get a piece of the China growth story, Alibaba could be something to look into.

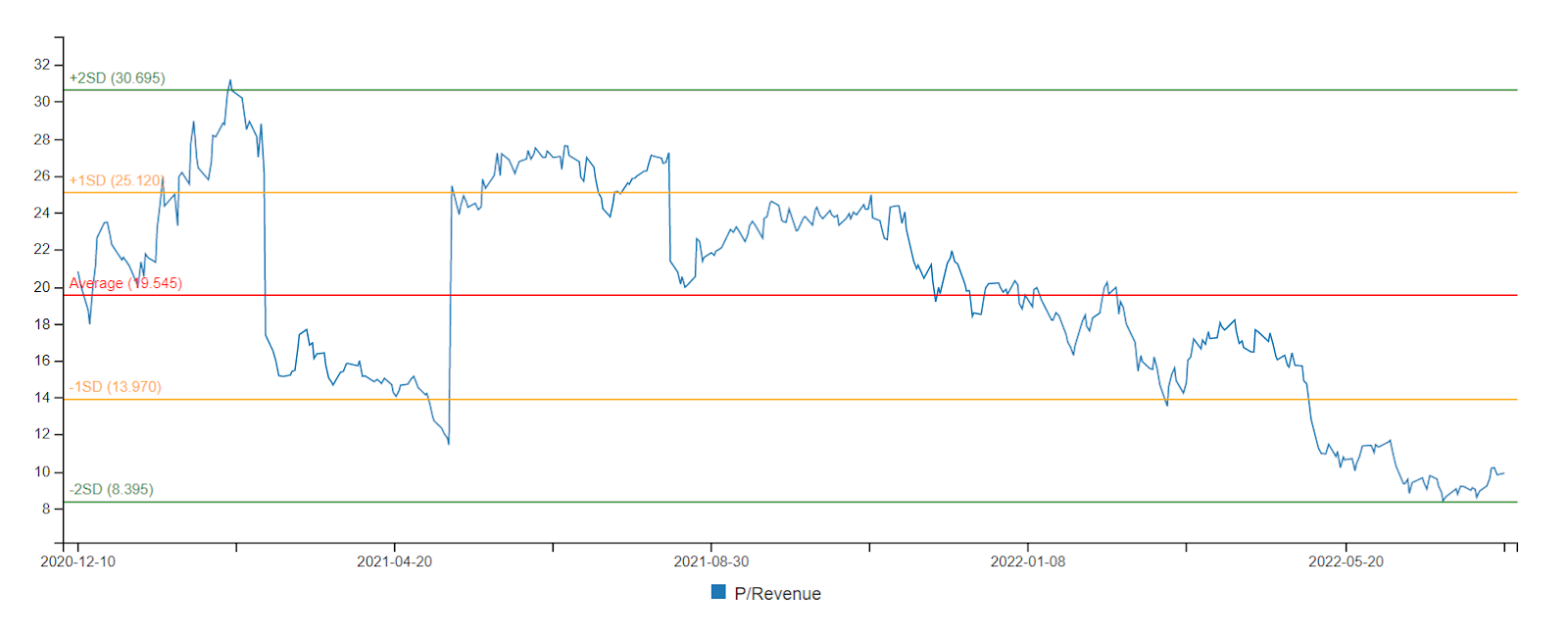

At Alibaba’s share price of US$103.96, it has a price-to-earnings (P/E) ratio of 31. Since 2017, the company’s average P/E ratio has been around 34x, suggesting that Alibaba is currently fairly valued.

VISA INC

You probably already have a Visa-enabled credit card in your wallet right now. The firm is one of the world’s largest electronic payments networks based on payments volume and number of transactions.

But many may not be aware that Visa does not issue credit cards nor extends credit, and therefore, does not work like a bank.

Visa is akin to a toll booth, and it collects a small fee for each transaction that passes through its payment network.

To use our Visa-enabled credit or debit card, four parties are involved, and they transact through Visa’s transaction processing network called VisaNet.

Here’s a diagram explaining the four parties and the role of each party:

The recurring revenue element from Visa is something that I like about the company, and its revenue growth has been extremely strong in the past.

Over the last 12 years, Visa’s revenue has stepped up from US$8.06 billion in FY2010 (financial year ended 30 September 2010) to US$24.11 billion in FY2021, translating to an annualised growth rate of 10.5%.

Due to operating leverage where expenses don’t scale up as much, net profit has grown at a faster rate of 13.8% annually, from US$2.96 billion to US$12.31 billion during the same time frame.

Visa has also posted strong free cash flow generation over the last 12 years, where the metric rose from US$2.45 billion in FY2010 to US$14.52 billion in FY2021.

Free cash flow is important for a company to be self-sustaining. Without any free cash flow, the business has to either borrow money from banks or undertake equity fundraising to sustain its daily operations.

The free cash flow of a company can be then used to reinvest into its own business, acquire other businesses, pay dividends to its shareholders, buy back its own shares, or pay off its borrowings.

Visa’s balance sheet is rock-solid as well. As of the end of FY2021, its total-debt-to-equity ratio stood at just 0.61.

For the company’s second quarter of FY2022, its net revenues and net income both grew on a year-on-year basis by 25% and 21%, respectively. Its total cross-border volume also rose by 38% year-on-year, showing the strength of the economy in general.

Looking ahead, Visa mentioned:

“E-commerce spend, both domestic and cross-border, has remained strong and stable relative to 2019 at well above the pre-COVID trend line even as pandemic effects fade, and we are assuming this will continue. In line with payments volumes, we expect processed transactions growth relative to 2019 to remain strong and stable with the variability largely driven by the extent to which small ticket card present everyday spend comes back.”

With the war against cash and people accustomed to buying things online, Visa should continue doing well over the long term.

At Visa’s share price of US$213.37, it has a P/E ratio of 34x (averaging around over 80x in the past five years) and a dividend yield of 0.5%.

Final Thoughts

All three stocks chosen by Temasek are businesses with good potential to be very valuable in the long run. We look forward to see how they will turn out.

Written by Sudhan P, in collaboration with StocksCafe.

Disclaimer: The content in this article (the “Information”) is not and shall not be construed as investment advice. This Information is meant to be informative and for general purposes only. Investment involves risk. Past performance is not indicative of future performance. Investors should refer to the offering documentation of the product(s) for detailed information (including risk factors) prior to investing in the product(s). If you have any query on the above information or any product offering documentation, you should seek independent professional advice.